USD

US Dollar · DXY Index

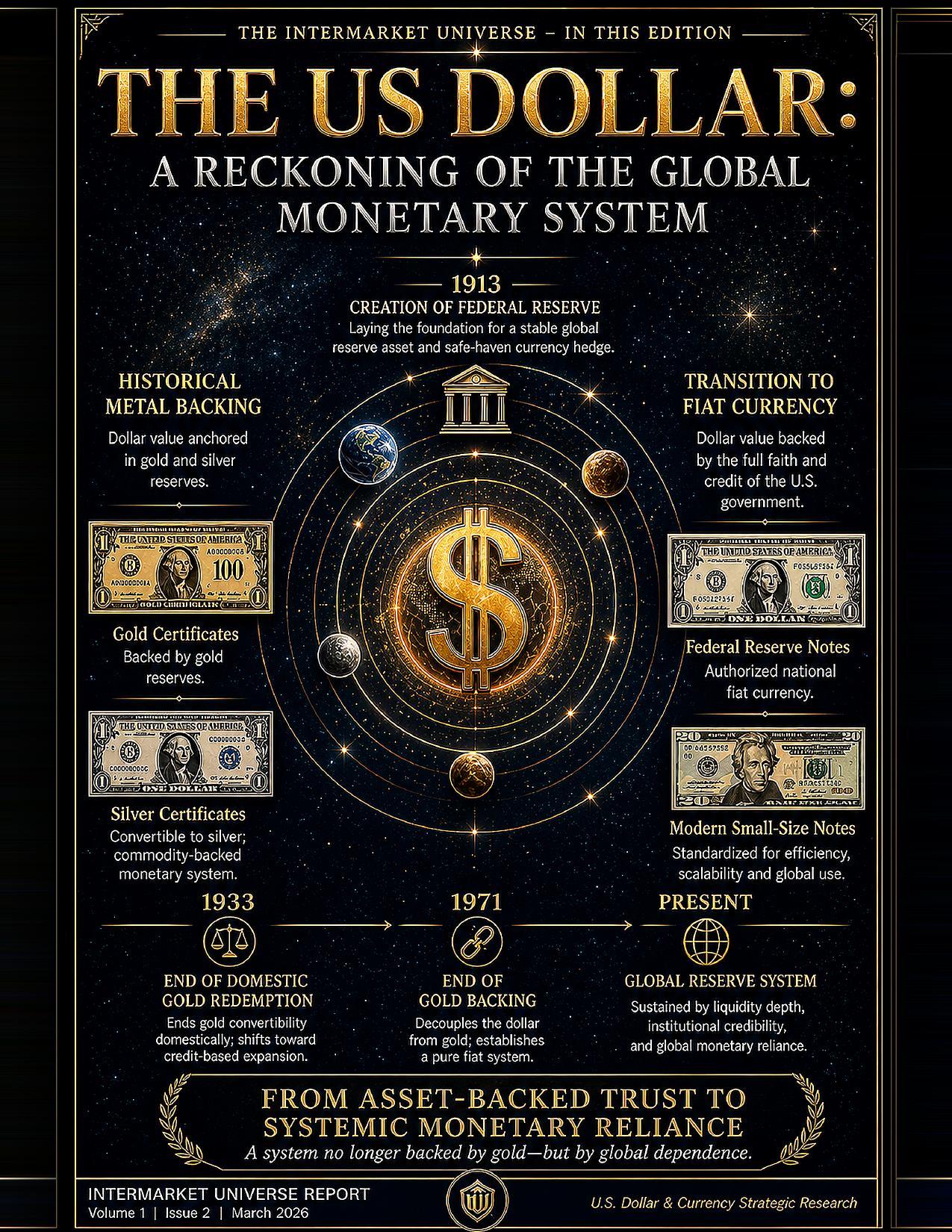

DXY −10%+ · 2025 · Fed Policy · Reserve Dynamics

Dollar Dominance at an Inflection: DXY Structural Outlook

Download PDF ↓

Institutional research newsletter on US dollar structural dynamics, DXY mechanics, reserve currency risk, and Fed policy divergence implications.