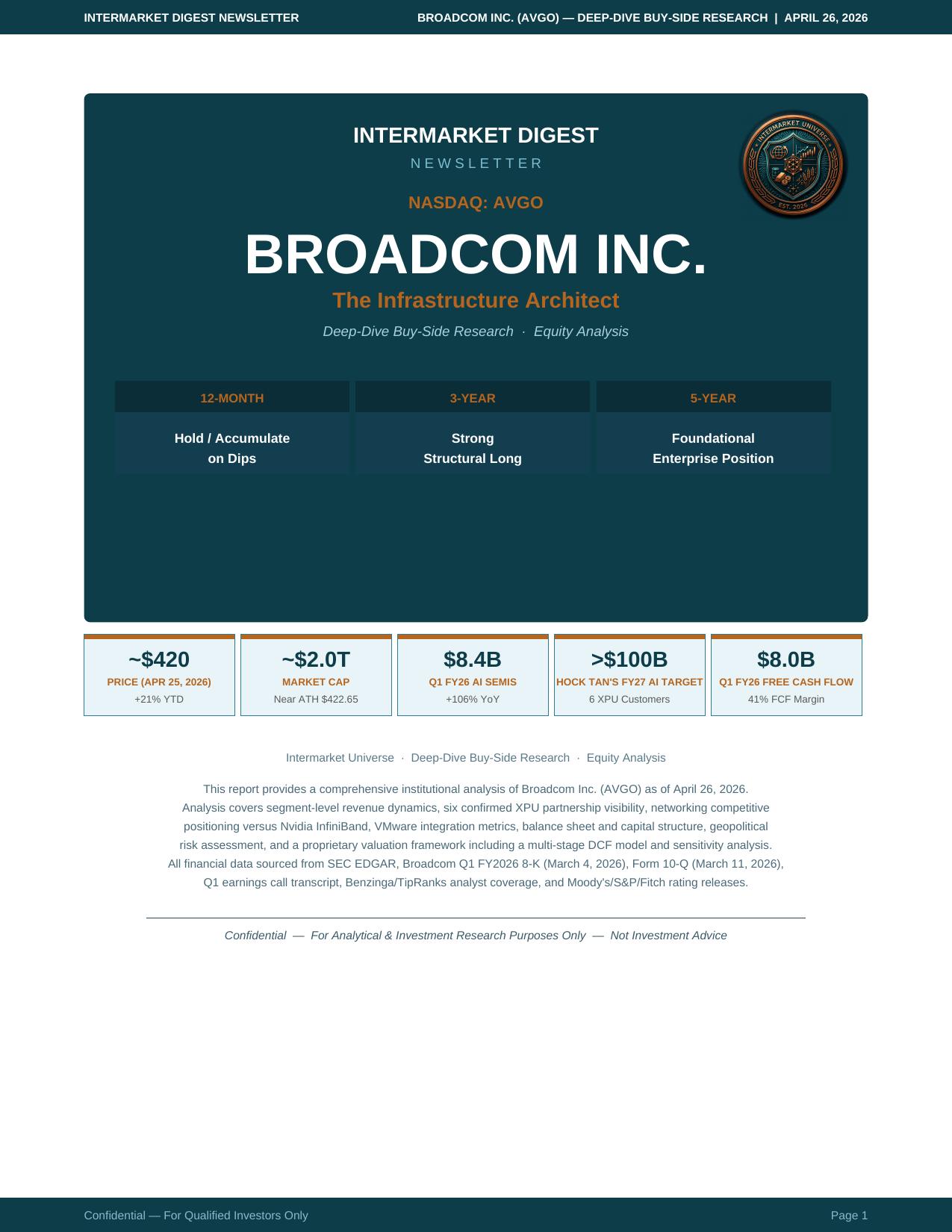

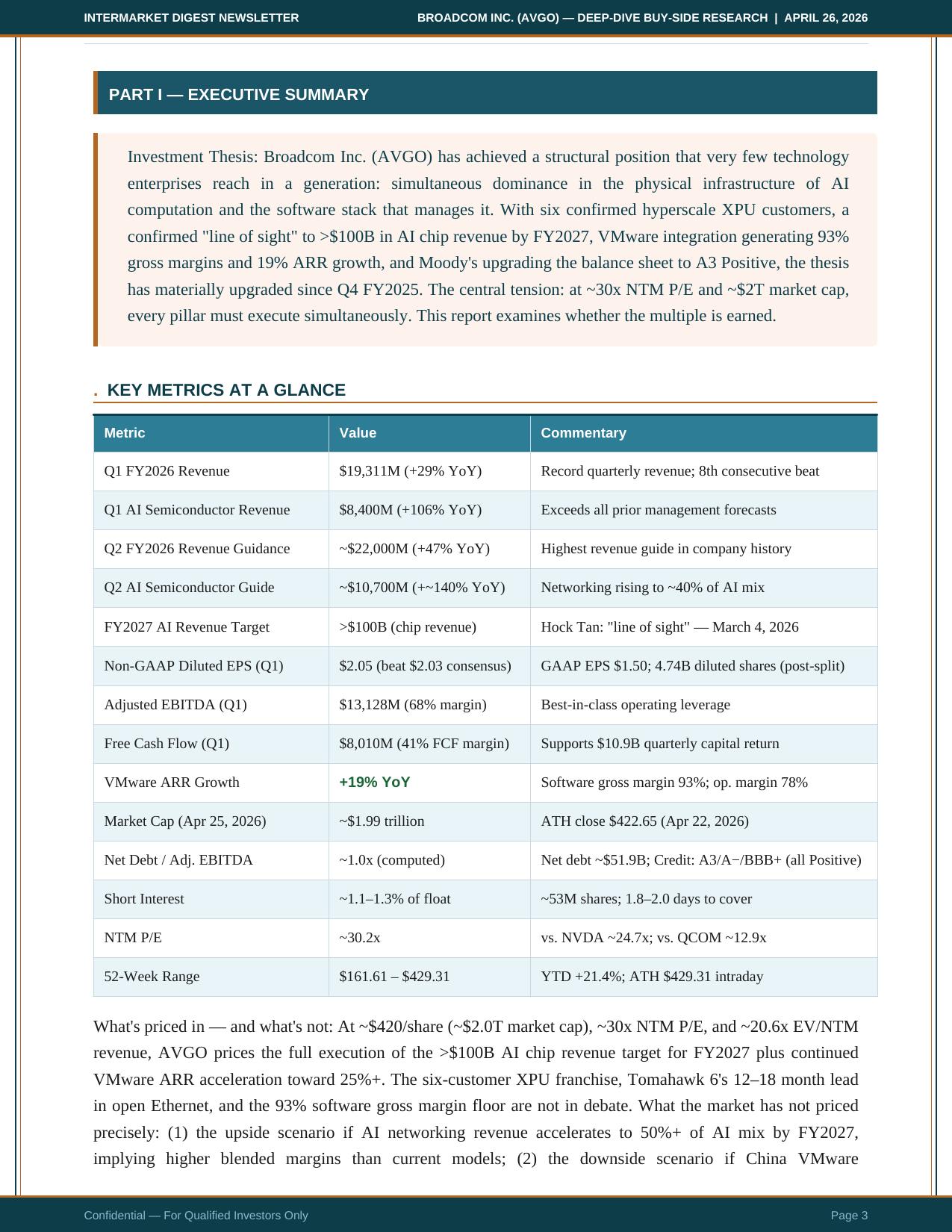

25-page institutional analysis covering Broadcom's dual-moat architecture — six confirmed XPU partnerships, Tomahawk 6 at 102.4 Tbps, VMware integration metrics, multi-stage DCF valuation, and three-horizon strategic positioning (12-month · 3-year · 5-year). Price as of April 25, 2026: ~$420. Market cap: ~$2.0T.